EU Fiscal Rules in 2026: What Member States Need to Know

- viopokhe

- 4 days ago

- 4 min read

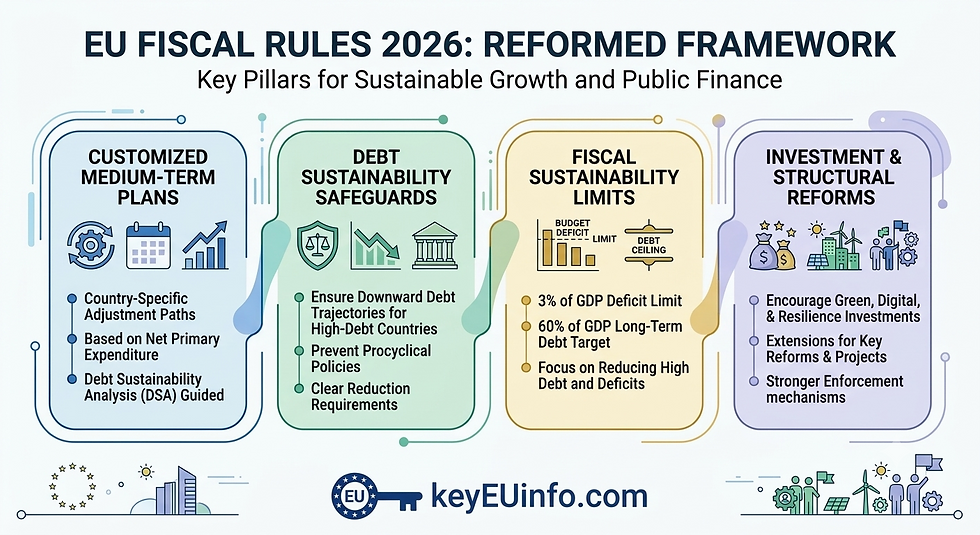

In 2026, EU fiscal rules are no longer just a technical topic for finance ministries: they directly shape national budgets, public investment plans, borrowing costs, tax policy, and the economic room available to governments. The reformed EU economic governance framework, in force since 2024, keeps the well-known reference values of a government deficit below 3% of GDP and public debt below 60% of GDP, but it changes how compliance is monitored and how fiscal adjustment is planned.

The key shift is from short-term annual targets to country-specific medium-term fiscal-structural plans. Each member state must follow a net expenditure path that reflects its debt sustainability, reform commitments, investment needs, and macroeconomic outlook. For 2026 budgets, this means governments must balance fiscal discipline with pressure to finance defence, energy security, green transition, digitalisation, social resilience, and competitiveness.

What Changed Under the New EU Fiscal Framework?

Policy area | Previous emphasis | 2026 practical focus |

Fiscal surveillance | Multiple indicators and annual assessments | Single operational focus on country-specific net expenditure paths |

Budget planning | Shorter-term adjustment targets | Medium-term fiscal-structural plans covering four to five years |

Debt control | Rules-based debt reduction benchmarks | Debt sustainability analysis with safeguards for high-debt countries |

Investment treatment | Limited room for reform-linked flexibility | Possible longer adjustment period where credible reforms and investments are committed |

Enforcement | Complex procedures with uneven compliance | Stronger monitoring of expenditure paths and national commitments |

The new framework is designed to be simpler in presentation but more tailored in application. Instead of applying the same adjustment logic to every member state, the European Commission assesses each country’s debt sustainability and provides guidance on the maximum growth of net expenditure. This makes the system more realistic for countries with different debt levels, growth prospects, demographic pressures, and investment needs.

For member states, the 2026 challenge is implementation. A government may want to cut taxes, increase wages, expand subsidies, or invest in infrastructure, but those decisions must fit within the agreed expenditure path. Countries with high debt or deficits above the Treaty reference values will face tighter scrutiny, while countries with healthier public finances still need to preserve fiscal buffers for future shocks.

Key Fiscal Rules and 2026 Budget Implications

Rule or mechanism | What it means | Impact on member states in 2026 |

3% deficit reference value | Government deficit should remain below 3% of GDP or be brought below it. | Limits room for unfunded tax cuts, subsidies, and spending increases. |

60% debt reference value | Public debt should remain below 60% of GDP or move toward a sustainable path. | High-debt countries may need multi-year consolidation plans. |

Net expenditure path | Annual growth of nationally financed net expenditure becomes the main control indicator. | Budget decisions must be checked against the agreed medium-term spending ceiling. |

Medium-term fiscal-structural plan | Each country sets a fiscal trajectory plus reform and investment commitments. | National budgets need to align with EU-approved multi-year plans. |

Adjustment period | Standard adjustment is usually four years, with possible extension to seven years. | Credible reforms and investments can reduce annual consolidation pressure. |

Excessive deficit procedure | Countries breaching deficit rules may face corrective monitoring. | Governments may need corrective fiscal measures and tighter budget execution. |

The net expenditure path is especially important because it focuses on spending that governments can control, net of certain revenue measures and cyclical items. In practice, it gives finance ministries a ceiling for policy choices: if a government introduces a permanent tax cut, raises public wages, or expands social transfers, it must show how the measure fits within the path or how it will be offset.

What Finance Ministries Should Watch in 2026

· Budget credibility: Fiscal plans should be based on realistic growth, inflation, interest-rate, and revenue assumptions.

· Debt sustainability: High-debt countries need clear paths showing how debt will decline or remain prudent over time.

· Public investment protection: Governments must avoid cutting productive investment simply to meet short-term expenditure limits.

· Tax-policy consistency: New tax cuts, exemptions, or windfall measures should be tested against medium-term fiscal commitments.

· EU funding absorption: Recovery, cohesion, defence, and green-transition funds should be coordinated with national budget planning.

· Compliance monitoring: Deviations from the agreed expenditure path can trigger EU scrutiny and market concerns.

The fiscal rules also matter for businesses and investors. If governments need to consolidate, companies may see changes in corporate taxation, VAT policy, excise duties, sector-specific levies, subsidies, wage support, public procurement, or infrastructure spending. In higher-debt countries, 2026 may bring more careful screening of new fiscal measures and a stronger preference for targeted, temporary, or EU-funded programs.

At the same time, fiscal consolidation does not automatically mean austerity. The new framework gives governments space to combine adjustment with growth-enhancing reforms and investments, especially where those reforms support productivity, labour-market participation, energy independence, digital infrastructure, or defence capacity. The policy challenge is to make spending more selective, measurable, and aligned with EU priorities.

EU fiscal rules in 2026 require member states to think beyond annual budgets and manage public finances through credible medium-term plans. The familiar 3% deficit and 60% debt thresholds remain important, but the operational focus has shifted to net expenditure paths, debt sustainability, reforms, and investment commitments. For governments, the priority is to preserve fiscal credibility while financing strategic needs; for businesses, the priority is to monitor how national budget choices may affect taxes, subsidies, procurement, and public investment.

FAQ about EU Fiscal Rules in 2026: What Member States Need to Know

What are the main EU fiscal limits in 2026?

Member states must keep or bring deficits below 3% of GDP and keep or move public debt toward the 60% of GDP reference value.

What is a net expenditure path?

A net expenditure path is the country-specific spending trajectory used as the main indicator for monitoring fiscal policy under the new rules.

Why do the rules matter for businesses?

They can influence tax policy, subsidies, public procurement, infrastructure spending, and the predictability of national budgets.

Can countries receive more time for fiscal adjustment?

Yes, countries may receive a longer adjustment period when they commit to credible reforms and investments.

Does fiscal consolidation always mean spending cuts?

No, it can also involve targeted reforms, revenue measures, better spending efficiency, and protection of productive investment.

EU Fiscal Rules in 2026: What Member States Need to Know

Comments